Banks raise deposit interest rates

Franchise explosion in Vietnam

6 leading economic sectors in Central region

91.9% companies are optimistic about production activities in the last 6 months this year

CPTPP makes shift of Vietnam from deficit to surplus

From September 1, 2021, Circular 06/2021/TT-BLDTBXH amending a number of articles of Circular 59/2015/TT-BLDTBXH of the Minister of Labor, War Invalids and Social Affairs on detailed regulations and guiding the implementation of a number of articles of the Law on Social Insurance regarding compulsory social insurance which has officially taken effect (“Circular 06”).

Accordingly, Circular 06 has clarified the condition that male employees are entitled to a one-time allowance when their wives give birth, which is stipulated in Article 38 of the Law on Social Insurance. Specifically, Clause 5, Article 1 of Circular 06 stipulates:

“In case the mother participates in social insurance but is not eligible to receive maternity benefits when giving birth, while the father has enough time to pay insurance then the father is entitled to a one-time allowance according to the statutory rate.”

Inside:

The mother participates in social insurance but is not eligible to receive maternity benefits: are the following cases (Not satisfying Article 31 of the Law on Social Insurance).

• Female workers giving birth; surrogacy and ask for surrogacy; Adoption of a child under 6 months of age paying social insurance premiums for less than 6 months during the 12 months before giving birth or adopting a child.

• Female employees who give birth while pregnant must take time off work to take care of the pregnancy under the direction of a competent medical examination and treatment facility paying social insurance premiums for less than 3 months in the 12 months before giving birth.

Time to pay insurance: Male employees must pay social insurance premiums for full 06 months or more within 12 months before giving birth; The husband of the mother who asks for surrogacy must pay social insurance premiums for full 06 months or more within 12 months up to the time of receiving the child.

The statutory rate: 02 times the base salary in the month of childbirth for each child.

Circular 06 takes effect from September 1, 2021.

Hope the above information is helpful to The Esteemed Readers.

Bizlawyer is pleased to accompany The Esteemed Readers!

On August 24, 2021, the Vietnam General Confederation of Labor issued Decision No. 3089/QD-TLD in 2021 on support meals for union members and employees who are doing “3 on-the-spot” activities of enterprises in the provinces and cities that implement social distancing in the whole province and city according to Directive 16/CT-TTg. Accordingly, this Decision stipulates the specific meal support level as follows:

• Objects entitled to suppor: Union members and employees working at enterprises paying trade union fees, doing “3-on-the-spot” for production.

• Support level: 1,000,000 VND/person, 1 time support.

• Time to implement support: Calculated from the effective date of the Decision – August 24, 2021

• Funding for implementation:

1. Support is provided to the grassroots trade union by the direct superior trade union from the unit’s accumulated financial resources. In case the immediate superior trade union does not have enough resources to provide support, then the Labor Confederation of provinces and cities; Central trade union and equivalent; Corporation’s Trade Union under the General Confederation shall cover.

2. The Labor Confederation of provinces and cities; Central trade union and equivalent; Corporation’s Trade Union under the General Confederation provide support to the superior trade union directly from the entity’s accumulated financial resources still in use at the time of grant. The case of The Labor Confederation of provinces and cities; Central trade union and equivalent; Corporation’s Trade Union under the General Confederation do not have enough resources to supply it, the General Confederation shall compensate for it so that The Labor Confederation of provinces and cities; Central trade union and equivalent; Corporation’s Trade Union under the General Confederation shall provide enough for the direct superior trade union.

• Implementation:

1. Report the number of union members and employees mobilized by the enterprise to carry out “3-on-the-spot” maintenance of production:

The grassroots trade union reports the quantity to the immediate superior trade union at the grassroots level for funding appraisal;

In case the enterprise has paid trade union fees but has not organized a trade union, the immediate superior trade union working with the enterprise shall check and determine the number of union members and employees.

2. Request for support:

The immediate superior Trade Union at the grassroots level proposes the Provincial and City Labor Confederation; Central trade union and equivalent; The Corporation’s Trade Union under the General Confederation provides support when the source cannot be balanced.

Labor Confederation of provinces and cities; Central trade union and equivalent; The Corporation’s Trade Union under the General Confederation requests the General Confederation to provide support when the source cannot be balanced.

3. On the basis of the proposal of union members and employees, the grassroots trade union (The immediate superior Trade Union for enterprises without a trade union) agree with the business owner on the method of organization, meals, transfer funds to support enterprises to organize meals according to the general policies of enterprises; at the same time, the grassroots trade union (The immediate superior Trade Union for enterprises without a trade union) supervises the organization of meals and makes them public to union members and employees.

This decision takes effect from August 24, 2021.

On July 15, 2021, the Government issued Decree 69/2021/ND-CP on renovation and reconstruction of apartment buildings (“Decree 69”), this Decree replaces Decree 101/2015/ND-CP on renovation and reconstruction of apartment buildings (“Decree 101”).

The introduction of Decree 69 is expected to overcome the difficulties and backlogs that have not been resolved during the implementation of Decree 101 which have been raised by the Ministry of Construction in Official Dispatch No. 159/BXD-QLN dated June 28, 2019. Specifically:

“The Ministry of Construction still receives many opinions from businesses, associations, the press and especially the opinions of National Assembly deputies and voters nationwide regarding the implementation of renovation and reconstruction of old apartments in most localities, it is still slow, leading to the situation that many households are still living in severely damaged and in danger of collapse, do not guarantee the safety of the owners and users of the old apartment building.”

Following are the highlights of Decree 69:

1. Firstly, Decree 69 clearly stipulates the cases in which the apartment building “must” be demolished to rebuild the apartment building or build other works according to the planning (Article 5 of Decree 69).

2. Second, Decree 69 stipulates more clearly on compensation, support, resettlement, and arrangement of temporary accommodation for owners and users of apartment buildings. In which, there is a separate section to specify relevant regulations (From Article 20 to Article 24 of Decree 69):

– Principles and content of compensation, support, resettlement, and temporary accommodation arrangements for owners and users of the apartment building.

– Compensation, support, and resettlement plans for houses and construction works not under state ownership.

– Compensation, support, and resettlement plans for houses and construction work under state ownership.

– A plan for temporary accommodation for owners and users of the apartment building.

– Sign contracts to buy, rent, lease-purchase houses, and construction works for resettlement.

Decree 69 takes effect from September 1, 2021.

Hope the above information is helpful to The Esteemed Readers.

Bizlawyer is pleased to accompany The Esteemed Readers!

On August 23, 2021, the Governor of the State Bank of Vietnam issued Circular No. 13/2021/TT-NHNN amending and supplementing a number of articles of Circular No. 26/2013/TT-NHNN on the Service Fee Schedule for payment via the State Bank of Vietnam. Accordingly, this Circular stipulates the reduction of specific payment fees as follows:

50% discount on payment fees at 02 services in the Schedule “Transaction fees for payment via Interbank Electronic Payment System” from September 1, 2021, to the end of June 30, 2022, including:

• Charge for payment transactions performed via the high-value payment subsystem, specifically:

Applied to any payment order that the payment system receives before 3:30 pm every day: Reduce from 0.01% to 0.005% of the amount paid (1,000 VND/item at a minimum; 25,000 VND/item at maximum).

Applied to any payment order that the payment system receives from 3:30 pm to the time when the payment system stops receiving payment orders in a day: Reduce from 0.02% to 0.01% of the payment amount (2,000 VND/item at a minimum; 50,000 VND/item at maximum).

• Charge for payment transactions performed via the low-value payment subsystem is reduced from 2,000 VND/item to 1,000 VND/item.

This Circular takes effect from September 01, 2021.

On June 30, 2021, the Ministry of Natural Resources and Environment issued Circular No. 09/2021/TT-BTNMT amending some Articles of circulars elaborating and proving guidelines for Land Law. This document takes effect from September 1, 2021.

Accordingly, cases of transferring land-use rights without obtaining permission from competent state agencies but must register fluctuations include:

• Repurposing of land for annual plant farming land into other types of agriculture land, namely: Land for construction of greenhouses and other housing for crop production; land for construction of housing for livestock, poultry, and other lawful animals; and land for aquaculture for the purposes of study, research and experimentation;

• Repurposing of other lands for annual plant farming land farming and land for aquaculture into land for perennial plant farming;

• Repurposing of land for perennial plant farming into land for aquaculture and land for annual plant farming;

• Repurposing of residential land into non-agricultural land which is not the residential land;

• Repurposing of land for trading, service activities into land for non-agricultural business which is not the land for non-agricultural production base (Amendments); Repurposing of land for non-agricultural business which is not the land for non-agricultural production base and land for non-agricultural business into land for construction of non-business works.

Accordingly, Circular 09/2021/TT-BTNMT has removed the case “Repurposing of land for trading, service activities into land for non-agricultural production base” from the list of cases that do not require permission but must register fluctuations at Clause 1, Article 12 of the previous Circular 33/2017/TT-BTNMT, this adjustment is consistent with point g, Clause 1, Article 57 of the Land Law 2013.

On June 30, 2021, the Ministry of Natural Resources and Environment issued Circular No. 09/2021/TT-BTNMT amending and supplementing a number of articles of circulars detailing and guiding the implementation of the Land Law. This document takes effect from September 1, 2021.

According to Clause 5, Article 11 of Circular 09/2021/TT-BTNMT when the National Database on Population has shared and connected with data of sectors and fields, including the field of land and people when Going to do the procedures for land registration, land-attached assets, granting land use right certificates do not need to submit a copy of ID card, citizen’s identity, household registration book. Instead, people’s information will be extracted from the National Database on Population.

With this revised content, creating favorable conditions for people and even competent agencies to handle dossiers, and at the same time in line with the changing conditions of relevant policies in population management activities reside.

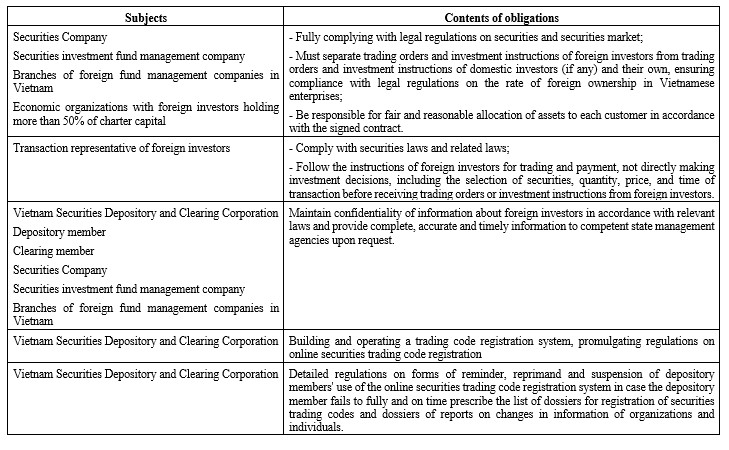

On June 30, 2021, the Ministry of Finance issued Circular 51/2021/TT-BTC guiding the obligations of organizations and individuals in foreign investment activities on the Vietnamese stock market, issued by the Minister of Finance (“Circular 51”). Circular 51 replaces Circular No. 123/2015/TT-BTC dated August 18, 2015 of the Minister of Finance guiding foreign investment activities on the Vietnamese stock market (“Circular 123”).

Circular 51 has introduced new reforms on obligations in providing services to foreign investors compared to the previous provisions in Circular 123. The following are highlights:

Circular 51 takes effect from August 16, 2021.

Hope the above information is helpful to The Esteemed Readers.

Bizlawyer is pleased to accompany with The Esteemed Readers!

On June 30, 2021, the Ministry of Finance issued Circular 51/2021/TT-BTC guiding the obligations of organizations and individuals in foreign investment activities on the Vietnamese stock market, issued by the Minister of Finance (“Circular 51”). Circular 51 replaces Circular No. 123/2015/TT-BTC dated August 18, 2015, of the Minister of Finance guiding foreign investment activities on the Vietnamese stock market (“Circular 123”).

Circular 51 has introduced new reforms on the reporting regime of entities in foreign investment activities on Vietnam’s stock market compared to the previous regulations in Circular 123. The following are highlights:

Note:

• Report recipient: State Securities Commission.

• At the request of the State Securities Commission, the subjects directly report and provide the list, data, and other documents related to the activities of foreign investors.

• Newspapers are presented in the form of paper documents attached to electronic data files or on the foreign investor activity management system of the State Securities Commission and must be archived for a minimum 5-year period of time.

Circular 51 takes effect from August 16, 2021.

Hope the above information is helpful to The Esteemed Readers.

Bizlawyer is pleased to accompany The Esteemed Readers!

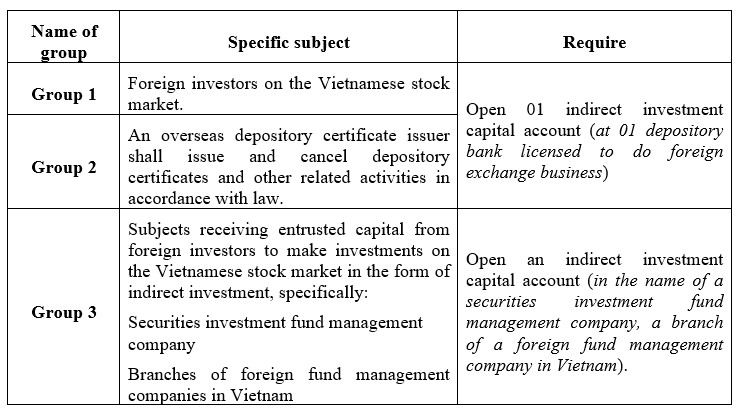

On June 30, 2021, the Ministry of Finance issued Circular 51/2021/TT-BTC guiding the obligations of organizations and individuals in foreign investment activities on the Vietnamese stock market, issued by the Minister of Finance (“Circular 51”). Circular 51 replaces Circular No. 123/2015/TT-BTC dated August 18, 2015, of the Minister of Finance guiding foreign investment activities on the Vietnamese stock market (“Circular 123”).

In addition to continuing to record the previous regulations in Circular 123 related to indirect investment accounts, Circular 51 has regulations to provide more detailed instructions on the groups of subjects that must open Indirect investment capital account when participating in and operating on the stock market, specifically includes the following 03 groups:

Note:

• All money transfer activities for carrying out transactions, investments, and other payments related to securities investment activities of foreign investors and activities of depository certificate issuers in foreign countries, receipt and use of dividends, distributed profits, purchase of foreign currency to transfer abroad (if any) and other related transactions must be done through the indirect investment capital account.

• The opening, closing, use, and management of indirect investment capital accounts comply with the law on foreign exchange management.

Circular 51 takes effect from August 16, 2021.

Hope the above information is helpful to The Esteemed Readers.

Bizlawyer is pleased to accompany The Esteemed Readers!