On September 17, 2021, the Ministry of Finance issued Circular 78/2021/TT-BTC guiding the implementation of the Law on Tax Administration, Decree 123/2020/ND-CP regulating invoices and documents (“Circular 78”).

One of the notable new points of Circular 78 is the provision on “Authorization for e-invoicing”: This means that sellers and service providers can authorize a third party to issue e-invoices for their selling goods and services. Here are the details.

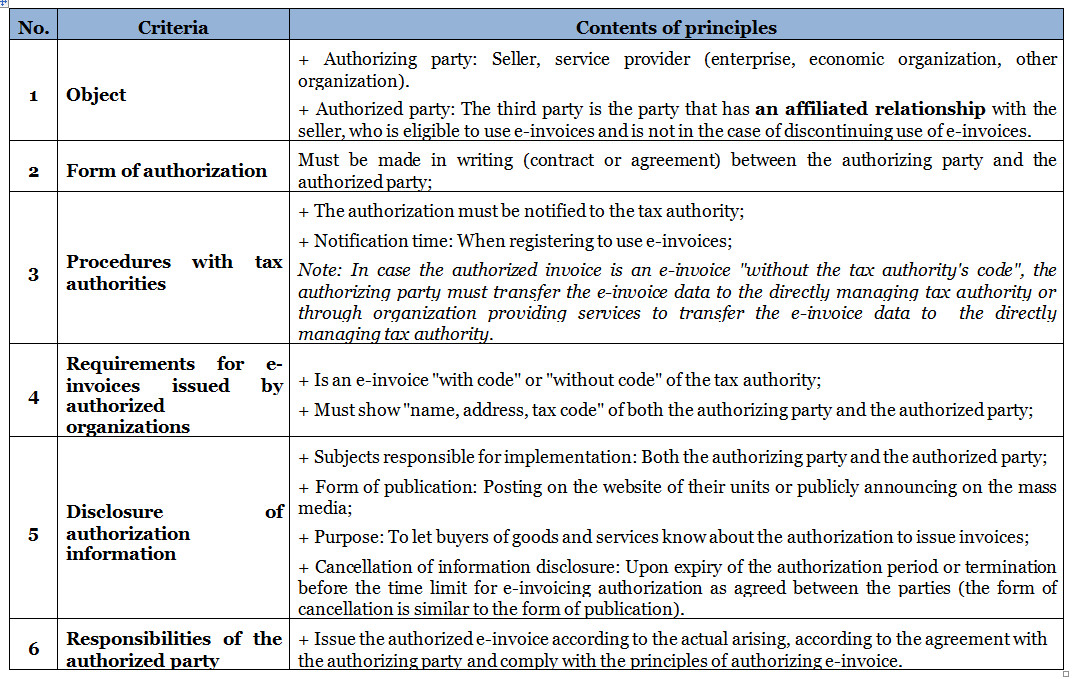

1. Principles of authorization for e-invoicing:

2. Authorization contract/Authorization agreement

– Content: Must fully show the following information:

a. Name, address, tax identification number, the ID number of the authorizing party and the authorized party;

b. Authorized e-invoices: invoice type, invoice symbol, invoice model number symbol;

c. Authorization purpose;

d. Authorization term;

e. Authorized invoice payment method (specify the responsibility to pay for goods and services on the authorized invoice);

– The authorizing party and the authorized party are responsible for storing the authorization document and presenting it when the competent authority requests it.

3. Notify the tax authority of the authorization to issue e-invoices

– The authorization is defined as the change of registration information for the use of e-invoices according to the provisions of Article 15 of Decree No. 123/2020/ND-CP. The authorizing party and the authorized party use Form No. 01DKTD/HDDT issued together with Decree No. 123/2020/ND-CP to notify the tax authority of the authorization to issue e-invoices, including the case of termination before the time limit for e-invoicing authorization as agreed between the parties;

– The authorizing party fills in the information of the authorized party, the authorized party fills in the information of the authorizing party in Form No. 01DKTD/HDDT issued together with Decree No. 123/2020/ND-CP.

Regulations on authorization to issue e-invoices have not been recorded in previous legal documents (Circular 119/2014/TT-BTC; Circular 26/2015/TT-BTC).

For more detailed information: The Esteemed Readers can refer to the provisions of Article 3 of Circular 78 and other relevant provisions. Circular 78 takes effect from July 1, 2022.

* This newsletter is only for informational purposes about newly issued legal regulations, not used to advise or apply to specific cases.

Hope the above information is helpful to The Esteemed Readers.

Bizlawyer is pleased to accompany The Esteemed Readers!

On October 20, 2021, the General Department of Customs issued Official Letter No. 4948/TCHQ-TXNK to give opinions on tax treatment for imported goods entrusted for export production. As follows:

– For goods imported for production and export:

(i) Raw materials, supplies (including those for the manufacture of packages of exports), components, semi-finished products imported incorporated into the exports or used during the manufacture of exports without being incorporated into the exports.

(ii) Finished products that are imported for packaging, labeling, or attaching to exports or packaging with exports as a whole.

(iii) Components and parts imported for the repair of exports under warranty.

(iv) Goods imported as samples that are not traded or used.

(v) Goods imported for manufacture of domestic exports but are permitted to be destroyed in Vietnam and have been destroyed in reality.

(According to the provisions of Clause 7 Article 16 of the Law on Import Tax and Export Tax No.107/2016/QH13, Article 12 of Decree No.134/2016/ND-CP dated September 1, 2016, as amended and supplemented at Clause 6 Article 1 of Decree No.18/2021/ND-CP)

Organizations and individuals that are eligible for import tax exemption for goods imported for production and export mentioned above but entrust other organizations and individuals (referred to as entrusted organizations or individuals) to import goods for export goods to be supplied to organizations or individuals entrusting the production of export goods, the goods imported by the entrusting organizations or individuals for the production of export goods shall be exempt from import tax provided that the supply of the prices of the goods are under the entrustment contract does not include import tax.

– Entrusting organizations and individuals are responsible for making announcements to production facilities and final settlement reports in accordance with the law.

– The inspection of production facilities shall be carried out by the customs authority for entrusting organizations and individuals.

This Official Letter takes effect from October 20, 2021.

On October 19, 2021, the National Assembly Standing Committee issued Resolution 406/NQ-UBTVQH15 in 2021 on a number of solutions to support enterprises and people affected by the COVID-19 epidemic. In particular, mention is made of tax exemption and reduction solutions for enterprises affected by the Covid-19 epidemic, specifically as follows:

(1) A reduction of 30% in the payable corporate income tax amount of 2021:

This tax reduction policy only applies to taxpayers under the provisions of the Law on Corporate Income Tax whose revenue in 2021 is not more than 200 billion VND and the revenue in 2021 is lower than the revenue in 2019.

* Note: The decrease in revenue in 2021 compared to the revenue in 2019 will not prevail as a criterion for reduction of paying corporate income tax if the taxpayer has just been established, engaged in consolidation, merger, partial division, or full division in the tax period of 2020 or 2021.

(2) Exemption of late payment interest incurred in 2020 and 2021 on debts of taxes, land use levies, and land rents to enterprises and organizations (including affiliated entities, places of business) that incur losses in 2020.

* Note: This provision does not apply to a case where the late payment interest has been paid.

(3) Apply reduction of value-added tax from November 1, 2021, to the end of December 31, 2021

– This policy applies to the following goods and services:

(i) Transport services (railway transport, water transport, aviation transport, other road transport); accommodation services; food and drink services; services of travel agencies, tour operators and support services, related to promotion and organization of tours;

(ii) Publishing products and services; cinematographic services, production of the television programs, sound recording and music publishing; works of art and services for composing, arts, and entertainment; services of libraries, archives, museums, and other cultural activities; sports, recreation, and entertainment services.

The goods and services mentioned in category (ii) do not include publishing software, and goods and services provided in the online form.

– The value-added tax reduction for the above cases is applied as follows:

(i) If the credit method is used, the enterprise will be eligible for a reduction of 30% in VAT rate;

(ii) If the direct method (payable VAT amount equals given rate multiplied by revenue) is used, the enterprise will be eligible for a reduction of 30% in the rate for direct VAT calculation.

This Resolution takes effect from October 19, 2021.

On October 8, 2021, the Government issued Resolution 126/NQ-CP in 2021 amending and supplementing Resolution 68/NQ-CP on a number of policies to support employees and employers who encounter difficulties due to the COVID-19 pandemic. Accordingly, the Resolution has amended regulations on the temporary suspension of contributions to the employer’s retirement and survivorship fund, specifically as follows:

– Regarding employers who have fully paid social insurance premiums or are temporarily suspending contributions to the retirement and survivorship fund until the end of January 2021 but have been affected by the COVID-19 pandemic, resulting in a downsizing of at least 10% of employees who have contributed to social insurance compared to January 2021 (including employees who stop working, suspend the performance of labor contracts and agreements on unpaid leave), the employees and the employers are entitled to a 6-month suspension of payment to the retirement and survivorship fund from the date of application submission.

– As for a case on the payment suspension under the Resolution No. 42/NQ-CP of April 9, 2020, and Resolution No.154/NQ-CP of October 19, 2020, of the Government, if the applicant is still qualified, the application will be approved as long as the suspension period does not exceed 12 months.

Thus, compared with the provisions of Resolution 68/NQ-CP, the amendments in this Resolution have extended the time limit for fully paying social insurance premiums or temporarily suspending payment to the retirement and survivorship fund of the employer (previously it was regulated until the end of April 2021) and the rate of reduction of employees participating in social insurance (previously it was regulated to decrease from 10% compared to April 2021).

This Resolution takes effect from October 8, 2021.

On October 8, 2021, the Government issued Resolution 126/NQ-CP in 2021 amending and supplementing Resolution 68/NQ-CP on a number of policies to support employees and employers who encounter difficulties due to the COVID-19 pandemic. Accordingly, the Resolution has amended and supplemented additional regulations for cases receiving support due to the impact of the Covid-19 pandemic, specifically as follows;

I. Expanding the beneficiaries of support upon the termination of labor contracts:

+ Employees working under labor contracts, participating in compulsory social insurance, must terminate labor contracts during the period from May 1, 2021, to the end of December 31, 2021, but not enough be eligible for unemployment benefits and fall under one of the following cases:

+ Must be in medical isolation, in blocked areas, or unable to go to the workplace due to the request of competent state agencies to prevent and control the COVID-19 epidemic;Due to the employer’s temporary suspension of operations at the request of a competent state agency for the prevention and control of the COVID-19 epidemic, or the head office, branch, representative office, production location, businesses in the area implement measures to prevent and control the epidemic according to the principles of Directive No. 16/CT-TTg or redeploy production and labor to prevent and control the COVID-19 epidemic.

II. Expanding the beneficiaries of support due to temporary suspension of labor contracts, unpaid leave:

Employees working under labor contracts, participating in compulsory social insurance up to the time immediately before suspending the performance of labor contracts, taking unpaid leave; there is a period of temporary suspension of the performance of the labor contract, taking unpaid leave within the term of the labor contract from 15 consecutive days or more from May 1, 2021, to the end of December 31, 2021, and The starting point of temporary suspension of performance of labor contracts, unpaid leave from May 1, 2021, to the end of December 31, 2021, and fall under one of the following cases:

+ Must be treated for COVID-19, medical isolation, in blocked areas, cannot go to the workplace due to the request of a competent state agency to prevent and control the COVID-19 epidemic;

+ Due to the employer’s temporary suspension of operations at the request of a competent state agency for the prevention and control of the COVID-19 epidemic, or the head office, branch, representative office, production location, businesses in the area to take measures to prevent and control the epidemic according to the principles of Directive No. 16/CT-TTg or redeploy production and labor to prevent and control the COVID-19 epidemic.

III. Expanding the beneficiaries of support due to job cessation:

Employees working under labor contracts who are terminated for reasons specified in Clause 3, Article 99 of the Labor Code; are participating in compulsory social insurance up to the time immediately before stopping work and fall under one of the following cases:

+ Having to be treated for COVID-19, medical isolation, in blocked or impossible areas to the working place at the request of a competent state agency according to the principles of Directive No.16/CT-TTg for 14 consecutive days or more during the period from May 1, 2021, to the end of December 31, 2021;

+ Due to the employer has to suspend operations at the request of a competent state agency or has a head office, branch, representative office, production or business location in the area to perform the following tasks: Measures to prevent and control the epidemic according to the principles of Directive No. 16/CT-TTg or redeploy production and labor to prevent and control the COVID-19 epidemic for 14 consecutive days or more during the period from May 1, 2021, to the end of December 31, 2021.

The level of support for the above subjects is applied as prescribed in Resolution 68/NQ-CP.

This Resolution takes effect from October 8, 2021.

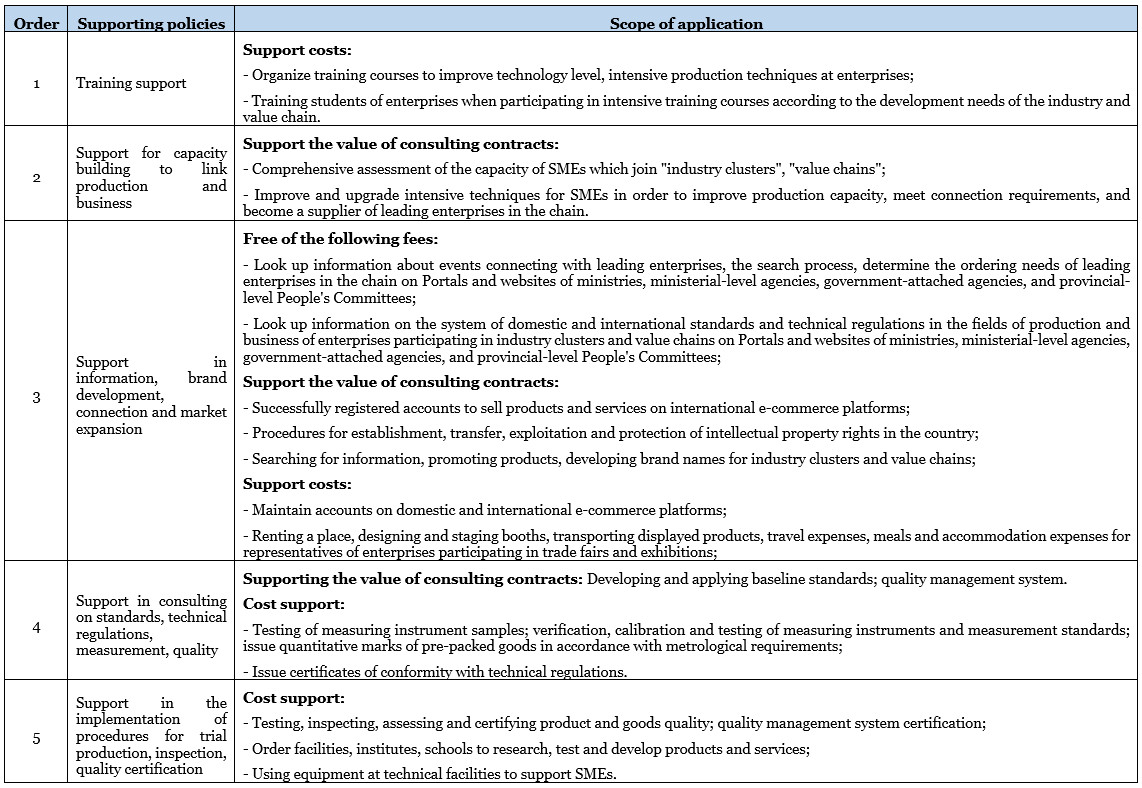

On August 26, 2021, the Government issued Decree No. 80/2021/ND-CP detailing and guiding the implementation of a number of articles of the Law on Supporting SMEs (“Decree No. 80”). Decree No. 80 replaces Decree No. 39/2018/ND-CP dated March 11, 2018, of the Government.

In the following, the article will review support policies “exclusively” for SMEs which join “industry clusters”, “value chains” in Decree No. 80, specifically as follows:

For details: Refer to the provisions from Article 25 of Decree No. 80.

Decree No. 80 takes effect from October 15, 2021.

Hope the above information is helpful to The Esteemed Readers.

Bizlawyer is pleased to accompany The Esteemed Readers!

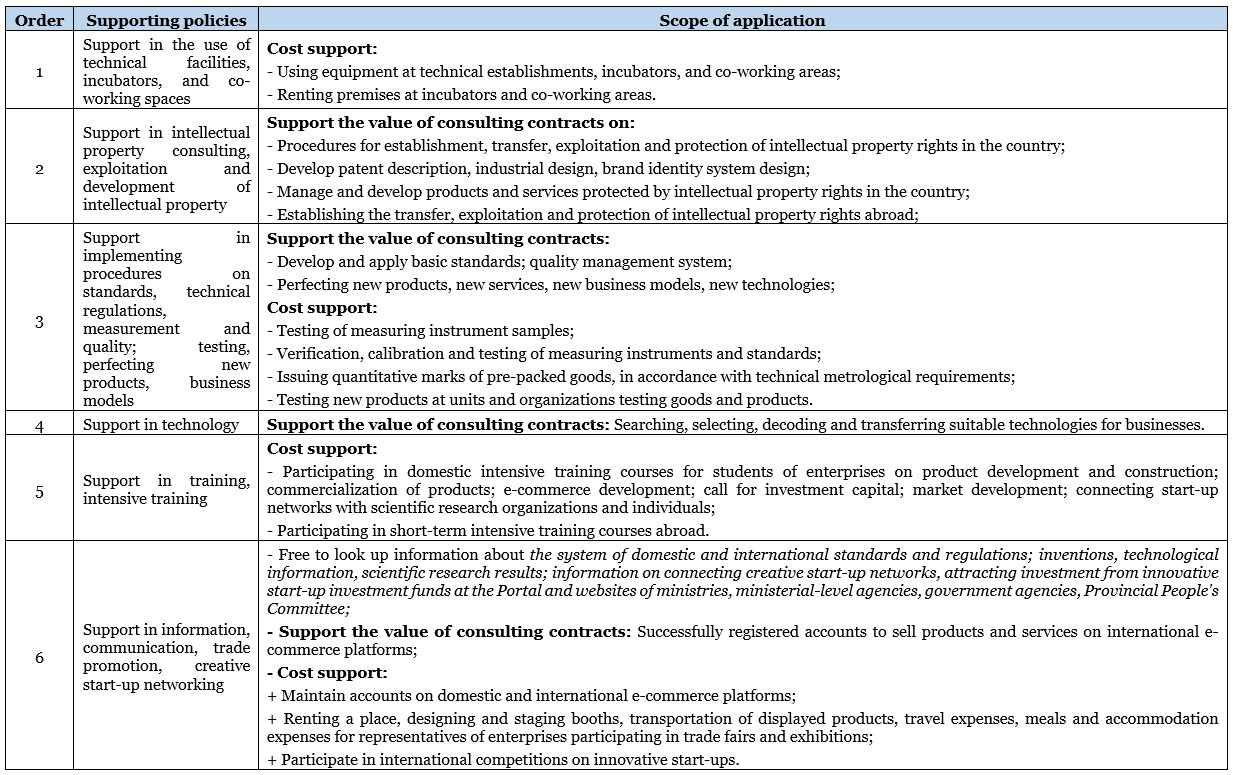

On August 26, 2021, the Government issued Decree No. 80/2021/ND-CP detailing and guiding the implementation of a number of articles of the Law on Supporting SMEs (“Decree No. 80”). Decree No. 80 replaces Decree No. 39/2018/ND-CP dated March 11, 2018, of the Government.

In the following, the article will review support policies “exclusively” for SMEs which are innovative startups in Decree No. 80, specifically as follows:

For details: Refer to the provisions from Article 22 of Decree No. 80.

Decree No. 80 takes effect from October 15, 2021.

Hope the above information is helpful to The Esteemed Readers.

Bizlawyer is pleased to accompany The Esteemed Readers!

In 2021, the Covid-19 epidemic has greatly affected the export and import activities of enterprises. Faced with that situation, some Customs Departments and the business community have proposed to consider not sanctioning administrative violations for a number of violations occurring in the customs field due to the impact of the Covid-19 epidemic and the Government’s application of social distancing and anti-epidemic measures, including the following cases:

1. Goods are on the list of goods subject to state inspection of quality, but foreign experts cannot come to Vietnam to assemble accessories for inspection of goods quality according to regulations.

2. Imported goods (chemicals) do not have tanks and cannot be consumed, so they must be stored at the port and cannot be declared at customs within the prescribed time limit.

3. The enterprise fails to submit the final settlement report, submits the report on the use of tax-free goods late due to social distancing, and does not have employees.

4. Enterprises cannot arrange financial resources to pay tax for all shipments that have returned to Vietnam within 30 days from the date of arrival at the border gate.

5. The enterprise cannot register the declaration and pick up the goods within 30 days from the date of arrival at the border gate due to the operation in the blocked area.

6. Enterprises cannot carry out re-export of goods under the Decision sanctioning administrative violations due to social distancing and the impact of the Covid-19 epidemic.

7. Enterprises cannot re-export and re-import goods within the prescribed time limit or on time for registration with the customs office due to social distancing and the impact of the Covid-19 epidemic.

8. Some customs units have F0 cases and practice social distancing, so they cannot make records of administrative violations receive dossiers, and exhibits of violations to verify and clarify violations for proper handling prescribed time limit.

Therefore, in order to create favorable conditions for enterprises with export and import activities, on September 15, 2021, the General Department of Customs issued Official Letter 4428/TCHQ-PC in 2021, requesting the customs authorities to review it. The consideration of not sanctioning administrative violations due to the influence of the Covid-19 epidemic and the Government’s application of social distancing and anti-epidemic measures must be based on the provisions of Articles 2 and 11 of the Law on Handling administrative violations in 2012, Article 6 of Decree 128/2020/ND-CP and specific case files to apply regulations related to “force majeure events” to each specific case.

Thus, in order to consider not sanctioning administrative violations due to the influence of the Covid-19 epidemic and to apply the Government’s social distancing and anti-epidemic measures, it is necessary to apply regulations related to “force majeure events” and individuals and organizations must prove that they have applied all necessary and permissible measures, but cannot prevent violations from occurring.

This Official Letter takes effect from September 15, 2021.

On September 16, 2021, the Minister of Health promulgated Circular No. 13/2021/TT-BYT stipulating the issuance of circulation numbers and the import of medical equipment to serve the prevention and control of COVID-19 in case of urgent.

Accordingly, medical equipment may apply the form of fast issuance of free registration numbers if the following conditions are satisfied at the same time:

As medical equipment for the prevention and control of the COVID-19 epidemic, the circulation number is quickly issued on the list of regulations, including Extraction machine; PCR machine, Chemicals (biological products) running the PCR machine for testing SARS-CoV-2; Rapid test kit for antigen/antibody against SARS-CoV-2; High-function ventilators, invasive and non-invasive ventilators, non-invasive ventilators, high-flow oxygen machines, portable ventilators; Continuous dialysis machine; Portable X-ray machine; Color Doppler ultrasound machine ≥ 3 probes; Blood gas meter (measuring electrolytes, lactate, hematocrit); Patient monitor ≥ 5 parameters; Electric injection pump; Infusion machine; Pacemaker defibrillators; ECG machine ≥ 6 channels; Portable ultrasound machine; Coagulation time meter; Hemodynamic meter.

Belongs to one of the following cases:

1. Has been approved for circulation or emergency use by one of the following organizations: US Food and Drug Administration (FDA) – USA; Therapeutic Goods Administration (TGA) – Australia; Health Canada (Health Canada); Japan’s Ministry of Health, Labor, and Welfare (MHLW) or Pharmaceuticals and Medical Devices Agency (PMDA) – Japan;

2. Has been approved by the competent authorities of the European countries for circulation and emergency use;

3. Belongs to the list of SARS-CoV-2 testing products for emergency use announced by the World Health Organization (WHO) on its website at https://extranet.who.int (Coronavirus disease) (COVID-19) Pandemic – Emergency Use Listing Procedure (EUL) open for IVDs | WHO – Prequalification of Medical Products (IVDs, Medicines, Vaccines, and Imm unification Devices, Vector Control);

4. Belongs to the list of popular products for testing for SARS-CoV-2 issued by the European Health Security Committee (EUHSC) published on its website at https:// ec.europa.eu (Technical working group on COVID-19 diagnostic tests | Public Health (europa.eu);

5. Having been granted a commercial import license in Vietnam before the effective date of this Circular (September 16, 2021);

6. Produced domestically in the form of technology transfer for medical equipment in one of the following cases (1), (2), (3), ( 4), (5) above;

7. Produced domestically in the form of processing for medical equipment in one of the following cases (1), (2), (3), (4), (5) above.

This Circular takes effect from September 16, 2021.

On August 25, 2021, the Minister of Construction issued Circular No.10/2021/TT-BXD guiding Decree 06/2021/ND-CP on quality management, construction, and Decree 44/2016/ND-CP on technical inspection of occupational safety.

Accordingly, this Circular details a number of contents on labor safety management, construction quality, and construction maintenance; applicable to domestic agencies, organizations, and individuals, and foreign organizations and individuals related to labor safety management, construction quality, and construction maintenance. Inside, the Circular has detailed instructions on the expenses of ensuring occupational safety and hygiene in the construction of works, including:

– Expenses for setting up and implementing safety measures;

– Expenses for training on occupational safety and health; expenses for technical inspection of occupational safety of machines and equipment; expenses for information and propaganda on occupational safety and health;

– Expenses for providing personal protective equipment and tools for employees;

– Expenses for fire and explosion prevention and fighting;

– Expenses for prevention and control of dangerous and harmful factors and improvement of working conditions; expenses of organizing risk assessment of occupational safety.

This is one of the contents of indirect expenses in the construction expenses of the work construction estimate.

This Circular takes effect from October 15, 2021.